The hidden risks around bank guarantee

Bank guarantees are considered quite a safe product. I try to break the myth by exploring the risky side from a ML/TF perspective.

Abhishek Dwivedi

8/13/20213 min read

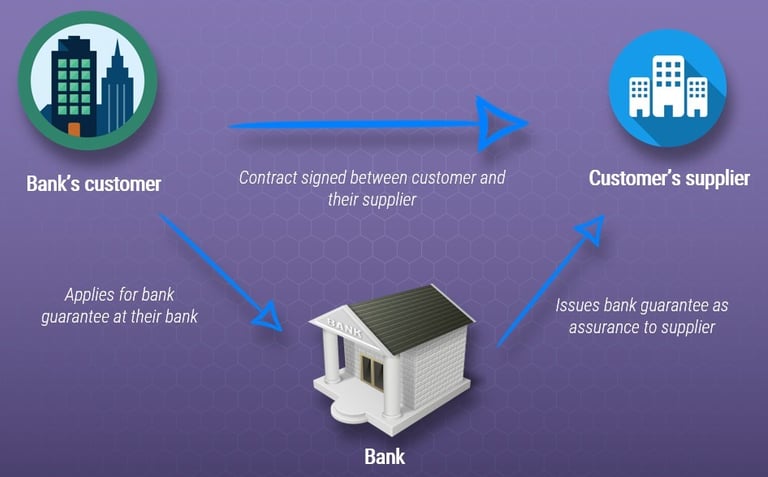

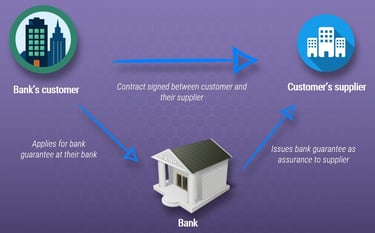

Several of my posts and articles come out of my practical experience in the AML/CFT space. While performing SIRA (or an AML risk assessment) and defining monitoring controls around identified risks, I have come across a simple looking and innocent product offered by banks - Bank guarantee! There are several flavours of this product but let's take a very basic usage as shown below :

A bank guarantees the supplier of their customer, that in case of a default, bank would assure the supplier gets the payment on time. The bank would then find a way to recover this money from their customer (in case the guarantee is called out). There are several types of guarantee based products which are used in the TCF and Lending space but the core concept remains the same.

Common perception

As you can imagine, such kind of product will only be used in case the customer fails to honor their obligations as laid down in the contract. A bank performs a thorough due-diligence before even issuing such a product to their customers so defaults are not expected either. Due to some of these reasons this product category is generally marked as a low risk. You will also come across statements such as the following during any ML/TF risk assessment discussions - "this product is rarely exercised", "in case of default everyone in product team is well aware","it will never happens for our customers" etc. etc.

Risks

You can understand the obvious reasons why the risks are considered to below. However I want to dig deeper on potential risks which you should be aware of, as these can go unnoticed.

In case of a default - In case you are the bank who has issued a guarantee, you need to be extra careful in cases of default. The documents prepared during the product issuance may (or may not) have listed the details of the beneficiary (e.g. the account number, destination of funds etc.). Once the guarantee is executed, you will be have to issue funds as per details of the beneficiary provided. You need to be extra careful on whether the intended beneficiary is indeed where the funds should end up. I have come across situations where, just before initiation of payment, the SSI (Standard Settlement Instructions) where updated to some different account (and the customer confirmed the same). This can be a risk as such last minute changes could be a red flag.

Intentional defaults - Imagine a situation where the customer intentionally defaults. The beneficiary will receive clean funds in their home bank account (and have a good story line) from your bank. Let's say your recovery process is to open a loan (equivalent to the funds issued to the beneficiary) in the name of customer. If the customer pays back this loan using dirty funds, your bank just became part of a well crafted scheme! Dirty money is used to pay off the loan where your bank ends up paying clean money to the beneficiary. In such situations you need to put extra checks on the recovery process (and activity of your customer around recovery process).

Beneficiary's angle - Considering this situation. Your customer keeps on receiving funds from another bank and their story for "source of funds" is the payment of default from a guarantee. If this happens once, probably fine, but if it's a regular activity, you need to dig a bit more deeper. There is a possibility that this customer of yours is listed as a beneficiary to several guarantees (at different banks) and a criminal syndicate has created a full-proof scheme where funds from high-risk countries easily end up at the beneficiary customer via a bank guarantee default scheme. In this situation you may have less to no insight about the guarantee itself, but the moment you get indiciation of a "guarantee default" payment, your alarm bells should start ringing.

Our team at Regxsa recently published a post on "Russian Laundromat" where bank guarantee was the vehicle used to move funds out of Russia! So take this product a bit more seriously than you assess by default ( as low risk). Hope this post gives some food for thought so you can consider your specific use case of the guarantee product and device ML/TF controls around it.